Options Alphas Pt. 1

We present 3 options alphas for trading BTC, ETH, SOL, and XRP

Introduction

In this article, the first in a three part series, we will present 3 working options alphas where we use options data to predict perpetual prices. Over the three articles we will present 5 alphas which achieve a combined performance above 2 Sharpe combined and 110 bps on dollars traded (All assets have sub-5 bps trading costs) on 72h rebalance (~1.5 Sharpe at 72h rebalance, ~2 Sharpe at 1h rebalance).

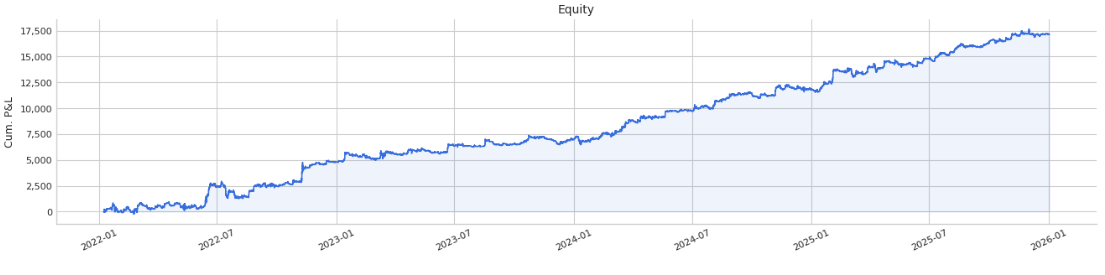

In the second article, we will share 2 more alphas ranging between 1 and 2 Sharpe, and show how to combine them. Then we will analyse the signal as a fully monetizable strategy in the 3rd article. These alphas use options data to predict perpetual prices of BTC, ETH, SOL, and XRP on Binance, one of the 3 we will present today is shown below:

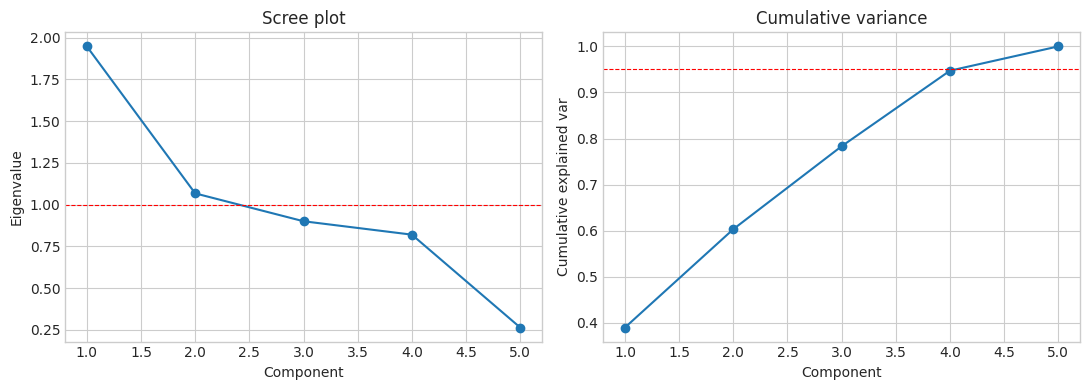

The alphas are fairly uncorrelated and orthogonal (not perfectly, but still very good for all being from the same dataset type) as seen in the scree plot below:

I think this series will be a real treat for readers as we present real working alpha which can actually be monetized now with no part left unexplained (other than data aggregation methods as this is very extensive, we will explain how to create the features of course though).

As with the previous article, I will not bore you with excessive writing as these are not complicated ideas and the work has already been done by myself in finding them, I will provide the feature, how to replicate it, and the performance.